Are Recoveries Slower After Financial Crises?

The reaction to the 2009 book This Time Is Different, by Carmen Reinhart and Kenneth Rogoff, is a case study in partisanship's effects on the interpretation of data. One idea from the book, that nations face an imminent debt crisis once public debt reaches 90 percent of Gross Domestic Product, permeated the right and was frequently cited by Tea Partiers as a motivation for their movement. Although that finding didn't carry as much weight on the left side of the aisle, another of Reinhart and Rogoff's conclusions did, namely that financial crises lead to longer recessions. It's regularly mentioned as an explanation for why the recovery during President Obama's office hasn't been stronger, including by the president himself.

In today's Wall Street Journal, Rutgers economist Michael Bordo challenges that second claim, writing that his own research shows that "U.S. business cycles going back more than a century show that deep recessions accompanied by financial crises are almost always followed by rapid recoveries." Bordo explains that Reinhart and Rogoff's data includes a number of episodes in countries that have little in common with the U.S. He also distinguishes between the time it takes for the economy to fully recover and the speed of the recovery once the recovery has started. Financial crises usually entail deeper recessions, meaning that it takes longer for the economy to return to its previous output even if the recovery is relatively strong.

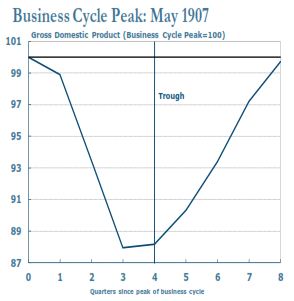

In Bordo's working paper written with Joseph Haubrich of the Federal Reserve Bank of Cleveland, he includes charts depicting U.S. recessions since the late 1800s to illustrate the pace of recoveries. For example, the 1907-08 recession was associated with a financial crisis, yet it was followed by a quick recovery:

Once the recovery began, the economy regained its previous level quickly, despite the preceding financial crisis.

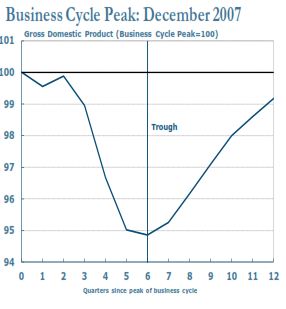

By contrast, the current recession featured a very sharp drop, followed by a shallower recovery (be sure to note the different scale on the x-axis):

In the past, Bordo's work has been referenced by the Romney campaign to pin the slow recovery on the Obama administration's policies, although Bordo pushed back against that interpretation. In today's WSJ piece, Bordo suggests that the cause of the economy's sluggishness can "largely be attributed to the unprecedented housing bust..." He doesn't rule out other possibilities, though: "Another problem may be uncertainty over changes in fiscal and regulatory policy, or over structural change in the economy."

Whether or not financial crises do indeed produce longer-lasting slowdowns, as the president and others have suggested, it's important not to confuse correlation for causality. It might be the case that in past recessions brought on by banking crashes, policymakers responded with harmful laws, leading to slower recoveries. President Obama, and Ben Bernanke for that matter, should not assume that a drawn-out, painstaking recovery is the only way forward.