The Conflicted Role of Proxy Advisors

Bottom Line: Proxy advisors, which provide institutional investors information and recommendations on shareholder votes, have immense influence over shareholder value and company policy and must be subject to basic oversight.

Institutional investors control a growing share of the publicly traded market. They rely upon external validators and resources provided by proxy firms to make data more digestible and assist in making shareholder investment and voting decisions.

These proxy firms, the largest of which are Institutional Shareholder Services (“ISS”) and Glass, Lewis & Co. (“Glass Lewis.”), provide analysis, recommendations, and consulting services on how annual and special proxies should be voted. Recommendations are issued on issues ranging from board appointments to acquisitions to environmental and social issues. Proxy advisors are able to significantly influence the direction of a company through their recommendations on shareholder proposals, Boards of Directors, or mergers and acquisitions.

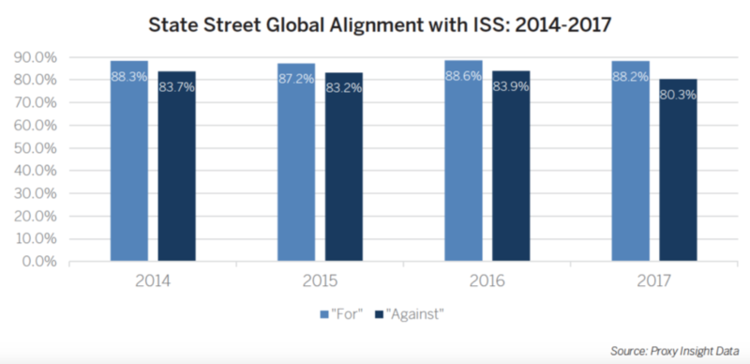

The large institutional investors they counsel own significant shareholdings in almost every major corporation and typically follow proxy advisors’ recommendations 80 percent of the time. This investor adherence gives proxy firms the power to act as quasi-regulators to require company disclosures not mandated by law.

While often characterized as “neutral” arbiters of good governance, proxy firms are for-profit enterprises. As a result, there is a conflict of interest between proxy advisors’ opinions and the interests of the companies that pay them the most.

Shifting policy changes demanded by proxy advisors create a hurdle for companies and a significant burden for small- and mid-cap companies that must constantly shift policy to comply with proxy advisors’ demands. This puts big businesses at a competitive advantage because they have the resources to comply.

Making matters worse, some hedge funds automatically and without evaluation rely on proxy firm recommendations, potentially breaching fiduciary duty, extending the influence of proxy firms, and making it more difficult for companies to defend their own positions.

It’s worth examining the biases, conflicts, and activism of these powerful institutions. In 2017, a federal bill introduced by Reps. Sean Duffy (R-WI) and Gregory Meeks (D-NY) proposed requiring proxy advisor firms to register with the SEC and comply with the regulations governing financial institutions. The bill passed the House of Representatives but has stalled in the Senate. Proxy advisory firms need regulatory oversight to ensure they are providing the same disclosure and transparency they often call for in the companies they evaluate.

Read the full report: “The Conflicted Role of Proxy Advisors” by Timothy M. Doyle, Vice President of Policy & General Counsel at the American Center for Capital Formation.