Ex-Im: Lessons From a Government Failure

Though it's been hibernating for the past three months, the Export-Import Bank may be on the cusp of revival. We learned on Friday that in the midst of the chaos surrounding the leadership vacuum in the House of Representatives, a group of congressmen plan to employ a rare procedural tactic to bring Ex-Im directly to the House floor without going through a committee. A vote is likely to come on October 26. Perhaps the best thing about this is that it will be a boon to civics teachers.

If you want to decode the mysteries of economics, shed light on the dark recesses of modern democracy, and get students excited about the power of ideas, I can think of no better teaching tool than the controversial federal agency.

Yes, I know. Even the bank's name sounds boring. And that is the first lesson.

Lesson 1: In politics, it's often what you don't see that matters.

Back in 1962, political scientists Peter Bachrach and Morton Baratz wrote an important article on political power. Their thesis was at once simple and profound: Power has two faces. The first face (or should we say talking head?) is what dominates observed public conflict. It concerns the highly salient issues that consume all of the oxygen in Washington. Think: immigration, the Iran deal, The Donald's latest insult. The second face of power — arguably the true face — is all about agenda-setting. It concerns the ability to keep certain items out of public scrutiny and not talked about. Think: the farm bill's rarely discussed orgy of privileges to some of the nation's wealthiest households, or the tax code's unquestioned preferences for high-income homeowners.

The more arcane, complex, and — yes — boring the policy, the easier it is for those who wield the second face of political power to keep the issue off the agenda. The Export-Import Bank is just such an issue. A relic of World War II, the federal agency was created to aid a country that no longer exists, the USSR. Now, the agency's main purpose is to subsidize ten highly profitable corporations, including Boeing, GE, Bechtel, Exon Mobile, and Caterpillar. In fact, about 35 percent of the agency's subsidies benefit just one company: Boeing.

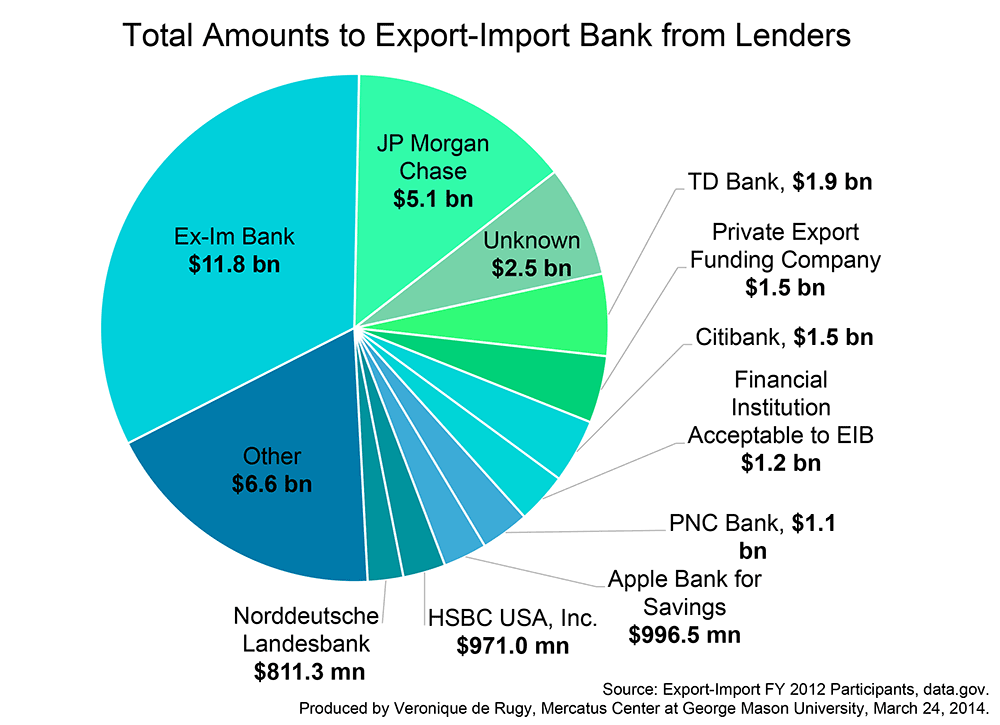

The agency privileges these firms by offering taxpayer-backed loan guarantees, working capital guarantees, direct loans, and export-credit insurance. At the moment, the agency's preferred form of subsidy is a loan guarantee. Here is how it works: When a U.S. manufacturer such as Boeing tries to sell a plane to a foreign-owned company such as Emirates Airline, a large bank such as JP Morgan usually finances the deal. But in the event that the foreign buyer defaults on its loan to JP Morgan, the Ex-Im Bank (quite generously) will cover up to 85 percent of the outstanding balance. The agency covers its day-to-day costs by charging fees to the foreign buyers. But when major defaults happen (and they have), the bank relies on U.S. taxpayers for support.

{kind=link}

Lesson 2: There is no such thing as a free lunch.

If you listen to the agency's staff and its boosters (which include the Chamber of Commerce and the National Association of Manufacturers), you'd think the Ex-Im Bank is all upside and no downside. Clearly, manufacturers like Boeing benefit from its programs. So do big banks like JP Morgan. Foreign buyers also benefit, unless the Ex-Im Bank's subsidies lure them into deals they can ill afford, as happened to Air Nauru a few years back.

But as any student of economics will tell you, there is no such thing as a free lunch. These benefits to manufacturers, buyers, and financiers are paid for by others. Namely: taxpayers, consumers, and other borrowers.

Taxpayers, of course, bear a risk — facing a cost of up to $2 billion between now and 2024, according to fair-value accounting estimates by the Congressional Budget Office.

Consumers bear a cost. Because the Ex-Im Bank artificially boosts demand for products such as aircraft, the agency's subsidies raise the prices of these items. Some of this cost is passed along to you and me when we buy airline tickets. And some of it is borne by the investors and employees of the airlines themselves. This is one reason why Delta — which buys Boeing planes — has complained about the Ex-Im Bank. Delta also doesn't like that the agency subsidizes foreign airlines with whom it competes.

And finally, other borrowers bear a cost. All else being equal, a bank like JP Morgan would prefer to finance the purchase of an airplane and pass along 85 percent of the risk to taxpayers, rather than finance a new startup and bear 100 percent of the risk itself. That means that some capital is inevitably channeled away from non-subsidized projects.

So which is greater: the benefits bestowed on a handful of major corporations and banks or the costs foisted on a large number of taxpayers, customers, and borrowers?

As demonstrated in a new paper by economists Robert Beekman and Brian Kench, the costs outweigh the benefits. Economists even have a colorful phrase for these excess costs. They call them "deadweight losses." And they can be quite substantial.

But beyond these traditional losses there are others. One is "rent seeking" loss. The money that a firm like Boeing makes from the Ex-Im Bank's support is known to economists as "rent." Rent has nothing to do with apartments. It's the term we economists use to describe the extra profit that one earns from an artificially contrived, exclusive benefit such as a subsidy. As the late economist Gordon Tullock demonstrated in a landmark series of articles, "rent seeking" is socially wasteful. Firms seeking rent will lobby. They'll donate to PACs. And they will change their production decisions to satisfy political desires instead of customer desires. All of this comes at a cost. The overwhelming weight of evidence suggests that rent-seeking societies are poor societies.

And as I argued in a piece called "Pathology of Privilege," other costs attend corporate favoritism as well. When firms are shielded from competition, they pay little attention to consumer desires or to production costs. They have little incentive to innovate and change. And their managers waste their entrepreneurial talents devising new ways to protect their privileged positions instead of new ways to create value. In short, I concluded, "government-granted privilege is an extraordinarily destructive force. It misdirects resources, impedes genuine economic progress, breeds corruption, and undermines the legitimacy of both the government and the private sector."

Lesson 3: Concentrated interests usually win.

If the Ex-Im Bank is so costly, why has the agency stuck around for so long? It's outlasted 13 presidents and 39 Congresses. What is its secret to longevity? The answer lies in a simple observation made by the economist Mancur Olson in an insightful though not particularly readable book first published a half-century ago. (For an accessible version of Olson's ideas, I'd highly recommend Jonathan Rauch's "Government's End.") Olson's insight begins with the observation that all collective action is costly. It takes time, money, and effort to set up a PAC, to lobby Congress, or to organize a series of campaign ads. What's more, those of us who stand to gain from such action can free-ride on the efforts of others. His next insight is that smaller and more concentrated groups (such as a handful of manufacturers) will tend to find it far easier to overcome the collective-action problem than a large and diffuse group of people (such as consumers, borrowers, or taxpayers).

To put it in stark terms: You, me, and some 321,000,000 other taxpayers, consumers, and borrowers each stand to gain by organizing political opposition to the Ex-Im Bank. But while the aggregate savings from eliminating the agency are large, the individual savings for any one of us are modest. And besides, that's a lot of cats to corral. In contrast, Boeing, GE, and JP Morgan each stand to gain billions by organizing political support for the Ex-Im Bank. And while their total gains are smaller than the combined losses of taxpayers, consumers, and borrowers, their individual gains are immense. What's more, they have only a few cats to corral, so it's relatively easy for them to get politically organized.

The lesson is that concentrated interests tend to prevail over diffuse interests.

Lesson 4: Ideas > interests.

The next lesson is that Lesson 3 is sometimes wrong. While concentrated interests are a formidable force, so too are ideas. And in the very long run, ideas can trump interests. Edward Lopez and Wayne Leighton explore this concept in their superb 2014 study of social change. Their book centers on a rare point of agreement between the intellectual arch-nemeses John Maynard Keynes and F.A. Hayek. Keynes wrote of "academic scribblers" whose ideas influenced kings and world leaders (who were themselves typically oblivious to this influence). And Hayek talked about the "intellectuals" who refined the ideas of academics and shaped them into social change. Both men believed that ideas — whether right or wrong — shape history.

In the last two years, a powerful idea has taken hold: Government favoritism is a deeply destructive phenomenon. This idea has been gestating for quite some time. It animated the Constitution's general welfare clause, conveying the quaint notion that government ought to serve the general welfare of the masses and not the specific welfare of special interests. It can also be found in the writings of progressives like Gabriel Kolko and Ralph Nader. And it appears in the thinking of free-market economists such as George Stigler and Milton Friedman. There was a time when even Barack Obama (then a senator) denounced corporate welfare, specifically singling out the Ex-Im Bank. But for much of the last century, the concentrated interests wielded the second face of power to keep this idea off of the agenda.

But now government favoritism is very much on the national political agenda. And the Ex-Im Bank, the obscure, boring federal agency that oversees complicated financial deals, is at the center of this discussion. Earlier this summer, for the first time in its 80 year history, the Ex-Im Bank's congressional authorization lapsed. And now nearly every presidential candidate has had to take a position on the Ex-Im Bank.

How did this happen? Ideas.

Politico just identified the 50 most influential "thinkers, doers, and visionaries transforming American politics" for 2015. The list is a who's who of Keynesian scribblers and Hayekian intellectuals. Among those recognized were my colleague Veronique de Rugy and my friend Timothy Carney. In articles, posts, interviews, testimony, charts, and more charts, these individuals have done more to shed light on the inefficiencies and inequities of the Ex-Im Bank than anyone else in the last eight decades. And their ideas are making a difference.

Lesson 5: Politics is messed up.

If political markets were efficient, the agency would be permanently shuttered. But the final lesson is that political markets are far from efficient. They do not maximize utility, as the economist would say. Predictably, the concentrated interests who benefit from the agency are working feverishly to see that it is reinstated.

This lesson is handed down to us by a generation of thinkers, including Gordon Tullock and the late Nobel Laureate James Buchanan. There are many reasons to believe that political markets are inefficient. The three most important, in my view, are externalities, "logrolling," and rational ignorance.

Most students of economics are familiar with private externalities, such as pollution from factories.

Unfortunately, most students are not taught that political markets almost always entail externalities as well, despite the fact that Tullock first pointed this out in 1959. Majorities routinely select policies without accounting for the costs that spill over onto minorities; representatives frequently buy local pork-barrel projects for their constituents and foist the costs onto the whole nation.

Political externalities are facilitated through vote-swap agreements or logrolls. Through such agreements, everyone in the majority agrees to support the concentrated interests of everyone else in the majority. This explains why Professor Thomas Stratmann has found that members representing dairy and sugar interests tend to vote for peanut interests, and vice versa.

Right now, the concentrated interests who benefit from the Ex-Im Bank are trying to arrange just such an agreement. This summer, the Senate voted to tie the Bank's reauthorization to the highway bill, and it is possible that is how it will ultimately pass. Members whose constituents include the handful of firms that reap the lion's share of the agency's benefits are hoping that in agreeing to support highways in other members' districts, they can bring home the bacon.

Now Ex-Im boosters are pushing another tactic, a rare legislative procedure known as a "discharge petition." It allows them to bypass the normal committee process and bring an Ex-Im vote to the House floor. Like so much in politics, the procedure takes advantage of what the political economist Anthony Downs called voters' "rational ignorance." Since most voters have very little influence over political outcomes, it makes no sense for them to invest time and effort in studying policy. Thus, 218 members of Congress can be expected to support a measure that will do more harm than good for their unsuspecting constituents.

Taxpayers, borrowers, consumers, and progress be damned. What a lesson.

— Matthew Mitchell is a senior research fellow and director of the Project for the Study of American Capitalism with the Mercatus Center at George Mason University, where he is also an adjunct professor of economics.