Does the Retirement System Screw the Poor?

It's fashionable to slam 401(k)s — and similar tax breaks for retirement savings — as a handout to the rich. People with higher incomes pay higher tax rates, and therefore benefit more from such perks. If you're in the 35 percent tax bracket, for example, you save 35 cents for every dollar you shelter from the IRS; if you're in the 10 percent bracket, you save just 10 cents.

Not so fast, says Peter J. Brady, an economist for the Investment Company Institute (the trade association for American investment funds) who has published a free e-book on the retirement system. The critics' argument misses two key features of 401(k)s, Brady writes: The retirement plans merely defer taxation, rather than eliminating it entirely; and they're part of a much bigger retirement system that includes Social Security. On the whole, Brady finds, the retirement system is progressive.

Brady analyzes retirement subsidies by simulating the lives of six imaginary Americans. Each earns a different annual salary, ranging from $21,000 to $243,000. All of them, however, aim to replace 94 percent of their earnings in retirement, so they save money in a 401(k) as needed to supplement their Social Security. (The richest investor manages to replace just 85 percent, owing to the contribution limit.) To see how these workers would have fared without government retirement benefits, Brady runs alternative scenarios where retirement savings are placed in taxable investment accounts instead.

401(k)s actually have three different effects. First, contributions reduce the saver's taxable income in the year they're made — the effect that critics fixate on. But second, interest that accumulates is not immediately subject to the income tax. (Brady argues that this actually equalizes the incentive to save between rich and poor: Otherwise, the income tax provides a disincentive for the rich to save. With a 25 percent income tax, a 6 percent rate of return becomes a 4.5 percent rate of return.) And third, distributions during retirement are taxed, which disproportionately affects the rich. Brady's poorest simulated investor pays no income tax at all in retirement.

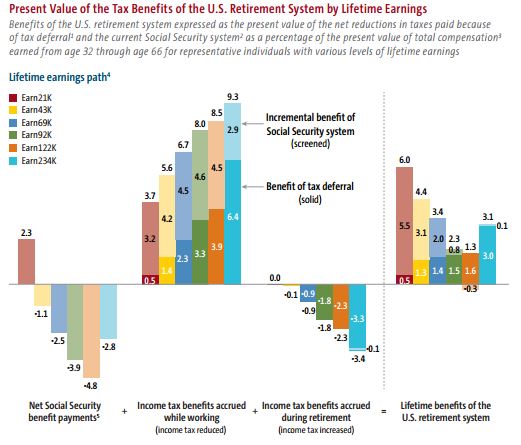

When all the effects are considered, the apparent unfairness of 401(k)s is diminished, though hardly eliminated:

Interestingly, in Brady's simulations, the rich benefit more because they save a lot more money, not because of their higher tax rates. Social Security replaces 67 percent of income for the poorest worker, but only 17 percent for the richest, so tax deferral plays a much larger role in the retirement plans of wealthier workers.

Which brings us to Brady's other key point: Tax deferral is just one part of the retirement system. When Social Security is brought into the analysis, it's clear that the poor actually gain the most, at least relative to their incomes:

Building on this observation, Brady cautions against worrying too much about the progressivity of any one component of our tax-and-transfer system. It's fine for a program to be regressive if that's what's necessary to achieve an important goal, so long as the system as a whole is satisfactorily progressive. (This is reminiscent of a point often made in an even broader context by the liberal Citizens for Tax Justice: While federal income taxes are quite progressive, state tax systems are often regressive. The two act in tandem to create a system that's not as progressive as you might think.)

At an event celebrating the book's debut, William Gale of the Brookings Institution laid out several criticisms of Brady's work, two of which are especially important. First, Brady's simulations overstate the system's progressivity in some ways — for example, they assume all workers save as much as they need to (up to the contribution limit) to replace 94 percent of their income, but in reality the poor and middle class are more likely to undersave or to lack benefits like 401(k)s. And second, progressivity is a rather weak demand to place on a retirement system; the true question might be whether the system is progressive enough.

Regardless, Brady lands some heavy blows upon critics of the retirement system. Apparently, it's not as bad as some thought. His book — which covers a lot of ground not explored above — is worth a close look.

Robert VerBruggen is editor of RealClearPolicy. Twitter: @RAVerBruggen