Social Security's Intergenerational Conundrum

Since its enactment in 1935, Social Security has become one of the most popular and effective federal programs. At the end of 2015, according to the recently published trustees’ report, 60 million Americans received retirement, disability, or survivors’ benefits from the system into which 169 million paid payroll taxes. Social Security provides the majority of cash income for 65 percent of elderly beneficiaries, makes up 90 percent or more of incomes for 36 percent of them, and offers the sole source of retirement income for 24 percent. The poverty rate among senior citizens is less than the poverty rate among working adults.

Yet, even as Social Security has become an indispensable source of financial wellbeing and security for the retired population, it has also become financially unsustainable in its current form.

Due to increasing lifespans and declining birth rates, there has been an apparently permanent shift in the ratio of working individuals to retiring baby boomers. Further, the program earns limited interest on its investment holdings. The Social Security trust funds have been running deficits since 2010 and are predicted to run out of cash reserves, which stood at $2.8 trillion at the end of April 2016, by 2034. Thereafter, only three-quarters of scheduled benefits can be paid for by the expected tax income.

Restoring solvency to the program will require either higher tax payments from current and future workers, or lower benefit payments — or, more likely, both. However it’s done, those receiving benefits in the future will pay more and get less compared to the beneficiaries now or in previous years.

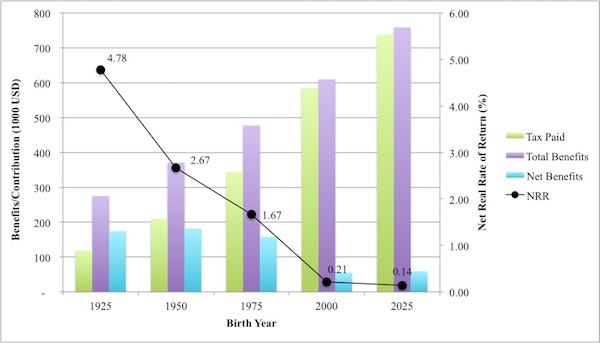

The unfairness for future generations can be seen in a simple, stylized example of the average wage earner. We calculated the net real rate of return (NRR) on lifetime payroll tax contributions for an average working male under the Old Age, Survivors and Disability Insurance (OASDI) program. The NRR is the real, average annual rate of return that tax contributions would have to earn to grow to a level sufficient at retirement to finance Social Security benefits for that worker until death.

In our calculations, we use the demographic and economic assumptions from the historical and long-term projections of the 2016 Social Security Trustees Report and supplementary data published by the Social Security Administration. Lifetime contributions and benefits for the retired, working, and future generations are computed using actual statutory tax rates and benefit formula. The 2016 report shows an actuarial deficit of 2.66 percent of taxable payroll. For simplicity, we assume that solvency is restored to the program by raising the payroll tax rate by that amount beginning in 2018. All amounts were set at constant 2016 dollars; amounts in the future were discounted at realized or expected real interest rates.

We calculated the NRR for a typical working male in five different generations, with birth years of 1925, 1950, 1975, 2000, and 2025. Workers are assumed to work every year starting age 23 until retirement at the normal retirement age, to be employed and earn the average wage in the economy each year, and to collect full scheduled benefits for the number of years equal to their period life expectancy at the age they retire. (The same methods and assumptions can be extended to study the effects of Social Security policy on people with various demographic and socioeconomic characteristics.)

The following figure shows the expected present value (at the normal retirement age) of payroll taxes paid over employed years and benefits received in retirement by average hypothetical workers.

Figure 1: Net Real Returns to Lifetime Contributions to Social Security (in 2016 dollars)

The earliest generations of Social Security beneficiaries enjoyed the highest rate of return. A worker born in 1925 who earned the average wage would have gotten a 4.8 percent return on their payroll taxes. The rate of return dropped to 2.7 percent for those born in 1950, and to 1.7 percent for those born in 1975. For those born in 2000 or 2025, the program is expected to provide a very low rate of return — less than .25 percent in both cases.

The trend is clear: over several decades, earlier cohorts of beneficiaries received benefits with an implied rate of return that would be viewed as sufficient for most retirement investments. But as changes have been made to the program, and the ratio of workers to retirees has declined, the trend has been toward higher taxes and benefits but a lower implied rate of return on lifetime payroll contributions.

The falling net rate of return for those entering the program in this century is a function of Social Security’s pay-as-you-go structure. Current workers pay the benefits for current retirees. That works well as long as the ratio of workers to retirees remains constant or rises. But when it falls — with declining birth rates and longer lives for retirees — it’s not politically feasible to take back benefits from those already in retirement. The only solution is to impose higher taxes and lower benefits on current and future workers.

This is Social Security’s intergenerational conundrum: the program is unsustainable in its current form, but it is too late to implement changes that will be fair across generations. The only way to restore the program to solvency is to impose changes that will lower the program’s returns to current and future workers who already get less relative to what they pay in compared to the program’s early entrants.

Of course, the rate of return a worker gets from Social Security can vary substantially within the same age cohort, due to various factors. The program also provides substantial redistribution from high to lower earners through its progressive benefit formula and important protections, e.g., for disability, which could not be replaced easily by private savings and insurance. Still, our simulations of the rate of return earned by the average worker are indicative of the overall trend across generations.

While insolvency is not imminent, we must act sooner rather than later to give these workers time to make the necessary adjustments in their retirement plans.

The goal of Social Security reform should be to ensure that the program can be sustained financially without undermining — and perhaps even improving — the program’s role as a floor of protection for older Americans. That can be done by reducing future benefits most for those with the highest wages; these workers can save more for their own retirement. Social Security’s limited resources could then be focused more on improving the standard of living for older Americans with limited lifetime earnings and thus also limited private savings.

The United States decided many years ago to run Social Security on a pay-as-you-go basis. For most of the program’s history, that decision posed no problems and, in fact, allowed for numerous benefit expansions as the workforce grew more rapidly than the retired population. But demographic shifts over the past half century have opened up a large projected funding gap that cannot be ignored. The gap is sizable, though it can be closed with reasonable program adjustments. The sooner Congress gets serious about taking the necessary steps to solve the problem, the better.

Tejesh Pradhan is a Ph.D. candidate in economics at American University and a Peterson Fiscal Intern at the Ethics and Public Policy Center. James C. Capretta is a resident fellow at the American Enterprise Institute.