Hedge Funds: A Bad Bet for Public Pensions

Public pension systems are now putting lots of money into hedge funds, hoping to earn higher returns and bolster their dangerously underfunded plans. But pension funds shouldn't be wasting resources on these expensive investments.

Hedge funds may indeed provide a worthwhile "hedge" during a stock-market decline -- their values tend to fall less than stocks' -- or if an extended period of low equity returns and high volatility ensues. But that advantage is more than wiped out when stocks experience their normal strong rebound, as has happened over the last seven years. For the long term, which is of overriding importance to pension funds, hedge funds are not the way to go.

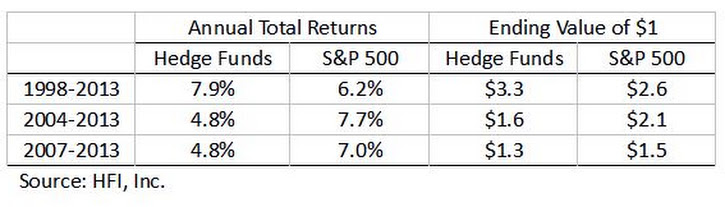

For the fifth consecutive year, hedge funds underperformed the stock market in 2013. Their average total return was 9.1 percent, versus 32.4 percent for the S&P 500. That makes the longer-term numbers look like this:

It's always hard to pick the right time frame for a fair comparison. We've shown three periods here. The first starts before hedge funds became broadly popular and had a brief period of really good performance. That is when David Swenson made hay for Yale. It also starts just as tech stocks began to gain great attention.

The second one starts after the stock market had experienced a strong rebound from the tech crash. And the third period, while rather short, has the classic fairness of going from one market peak to another.

The main conclusion from these numbers is that the big advantage of hedge funds is long over. More recently, passive portfolios of large-cap stocks have done much better, and these numbers do not even account for the huge difference in fees. True, the best hedge funds will likely continue to outperform the market. But they're hard to identify in advance and almost impossible to get into for all but the biggest and most prestigious accounts.

To a great extent, hedge funds' underperformance is due to the flood of money into the field and the proliferation of funds. Too much money -- and not just from pension funds -- is chasing the available smart trades. Thus, much of it goes into mediocre strategies or causes a drift in investment styles at otherwise shrewd firms that don't have the discipline to close their funds. Excessive inflows are a classic red flag for an investment strategy even before the bad numbers turn up.

A second factor working against hedge funds is that securities markets have been much more correlated -- that is, a decision to invest in one security instead of another matters less than it used to -- mainly because of the dominant influence of macro factors and government intervention on all markets since the recession. With less of a difference between various types of investments, there have been many fewer advantageous trading opportunities. Maybe someday the world will settle down, with smaller influences becoming more important again. But odds are that that time is some way off. With Europe still on its knees and trouble brewing in China, the kind of environment we've had since 2007 will likely persist.

Finally, many hedge funds are not really designed to hedge at all. Hedging is about reducing the potential downside on an investment to some preset risk level. Yet many, if not most, hedge funds are little more than glorified trading houses or mutual funds, at several times the cost. Their fee structures reflect it, incentivizing the chase for more assets and higher returns instead of accomplishing risk-management goals and consistent return targets.

For these reasons, hedge funds in general should be considered an unrewarding and risky arena. It's one that public pension funds should steer clear from.

Iliya Atanasov is a senior fellow on finance at Pioneer Institute, a Boston-based think tank, and H. Bradlee Perry is an investment consultant and advisor to Marble Harbor Investment Counsel.